pacman::p_load(sf, spdep, tmap, tidyverse)Hands-on Exercise 2 part 2

Global Measures of Spatial Autocorrelation

Overview

In this exercise we will utilise Global and Local Measure of Spatial Autocrrelation(GLSA). We will plot a Moran scatterplot and compute and plot the spatial correlogram. Additionally we will also compute the Local Indicator of Spatial Association(LISA)

Loading packages and data

Load packages

Load data

Here we will use the local development indicators of Hunan province, China, in 2012.

hunan <- st_read(dsn = "data/part 2/geospatial",

layer = "Hunan")Reading layer `Hunan' from data source

`C:\Users\Lian Khye\Desktop\MITB\Geospatial\geartooth\ISSS624\Hands-on_Ex02\data\part 2\geospatial'

using driver `ESRI Shapefile'

Simple feature collection with 88 features and 7 fields

Geometry type: POLYGON

Dimension: XY

Bounding box: xmin: 108.7831 ymin: 24.6342 xmax: 114.2544 ymax: 30.12812

Geodetic CRS: WGS 84hunan2012 <- read_csv("data/part 2/aspatial/Hunan_2012.csv")Rows: 88 Columns: 29

── Column specification ────────────────────────────────────────────────────────

Delimiter: ","

chr (2): County, City

dbl (27): avg_wage, deposite, FAI, Gov_Rev, Gov_Exp, GDP, GDPPC, GIO, Loan, ...

ℹ Use `spec()` to retrieve the full column specification for this data.

ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.Relational join of data

Here we will join the hunan2012 dataframe to the polygon or the hunan map. Bascially relating the development data to various regions of Hunan.

hunan <- left_join(hunan,hunan2012) %>%

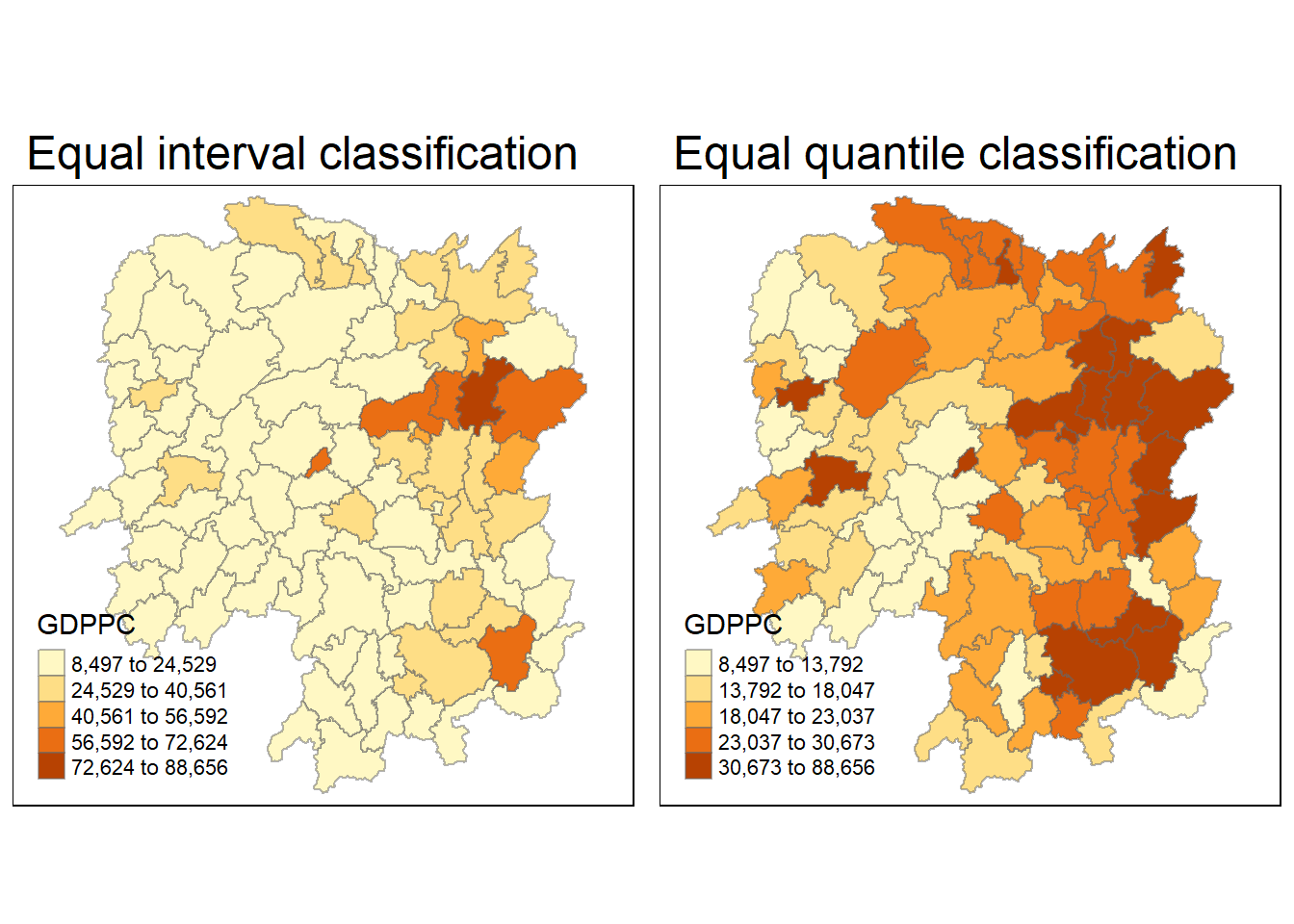

select(1:4, 7, 15)Joining with `by = join_by(County)`equal <- tm_shape(hunan) +

tm_fill("GDPPC",

n = 5,

style = "equal") +

tm_borders(alpha = 0.5) +

tm_layout(main.title = "Equal interval classification")

quantile <- tm_shape(hunan) +

tm_fill("GDPPC",

n = 5,

style = "quantile") +

tm_borders(alpha = 0.5) +

tm_layout(main.title = "Equal quantile classification")

tmap_arrange(equal,

quantile,

asp=1,

ncol=2)

Global Spatial Autocorrelation

Here we will compute global spatial autocorrelation statistics and perform a spatial complete randomness test.

Spatial autocorrelation describes the spatial relationship of variables and explore the statistical dependency of collection of variables in a region. These regions can refer to a continuous surface, fixed sites and areas that are dubdivisable.

Computing Contiguity Spatial Weights

We have to construct a spatial weights or to degine the relationships of the different regions. Here we will use the Queen contiguity weight matrix. Here we see if neighbours are similar to one another.

wm_q <- poly2nb(hunan,

queen=TRUE)

summary(wm_q)Neighbour list object:

Number of regions: 88

Number of nonzero links: 448

Percentage nonzero weights: 5.785124

Average number of links: 5.090909

Link number distribution:

1 2 3 4 5 6 7 8 9 11

2 2 12 16 24 14 11 4 2 1

2 least connected regions:

30 65 with 1 link

1 most connected region:

85 with 11 linksThe data shows that there are 88 regions. 1 region has 11 connected and immediate neighbours and 2 regions only having 1.

Row-standardised weight matrix

Next we will assign weights to each neighbour using equal weight. This is done using 1/number of neighbours. We will then sum up the weighted income values. This is to create proportional weights especially when the data contains unequal number of weights and is useful against potentially bias or skewed data.

rswm_q <- nb2listw(wm_q,

style="W",

zero.policy = TRUE)

rswm_qCharacteristics of weights list object:

Neighbour list object:

Number of regions: 88

Number of nonzero links: 448

Percentage nonzero weights: 5.785124

Average number of links: 5.090909

Weights style: W

Weights constants summary:

n nn S0 S1 S2

W 88 7744 88 37.86334 365.9147Global Spatial Autocorrelation using Moran’s I test

Moran’s I describes how features differ from the values in the study area as a whole. It uses a Moran I(Z-value).

I-value more than 0: Clustered and observations are similar.

I-value less than 0: Dispersed, observations tend to be different.

I-value close to 0: Random, scattered all over.

Performing the test

Here we use the moran.test() for calculating the Moran I value.

Null hypothesis or H0:

- observed pattern are equally likely as other pattern

- the value of one location is not dependent on neighbours

- changing the value of one region does not affect another

moran.test(hunan$GDPPC,

listw=rswm_q,

zero.policy = TRUE,

na.action=na.omit)

Moran I test under randomisation

data: hunan$GDPPC

weights: rswm_q

Moran I statistic standard deviate = 4.7351, p-value = 1.095e-06

alternative hypothesis: greater

sample estimates:

Moran I statistic Expectation Variance

0.300749970 -0.011494253 0.004348351 From the test above we can see that the Moran I statistical value is more than 0, meaning that the development of Hunan province has clustering.

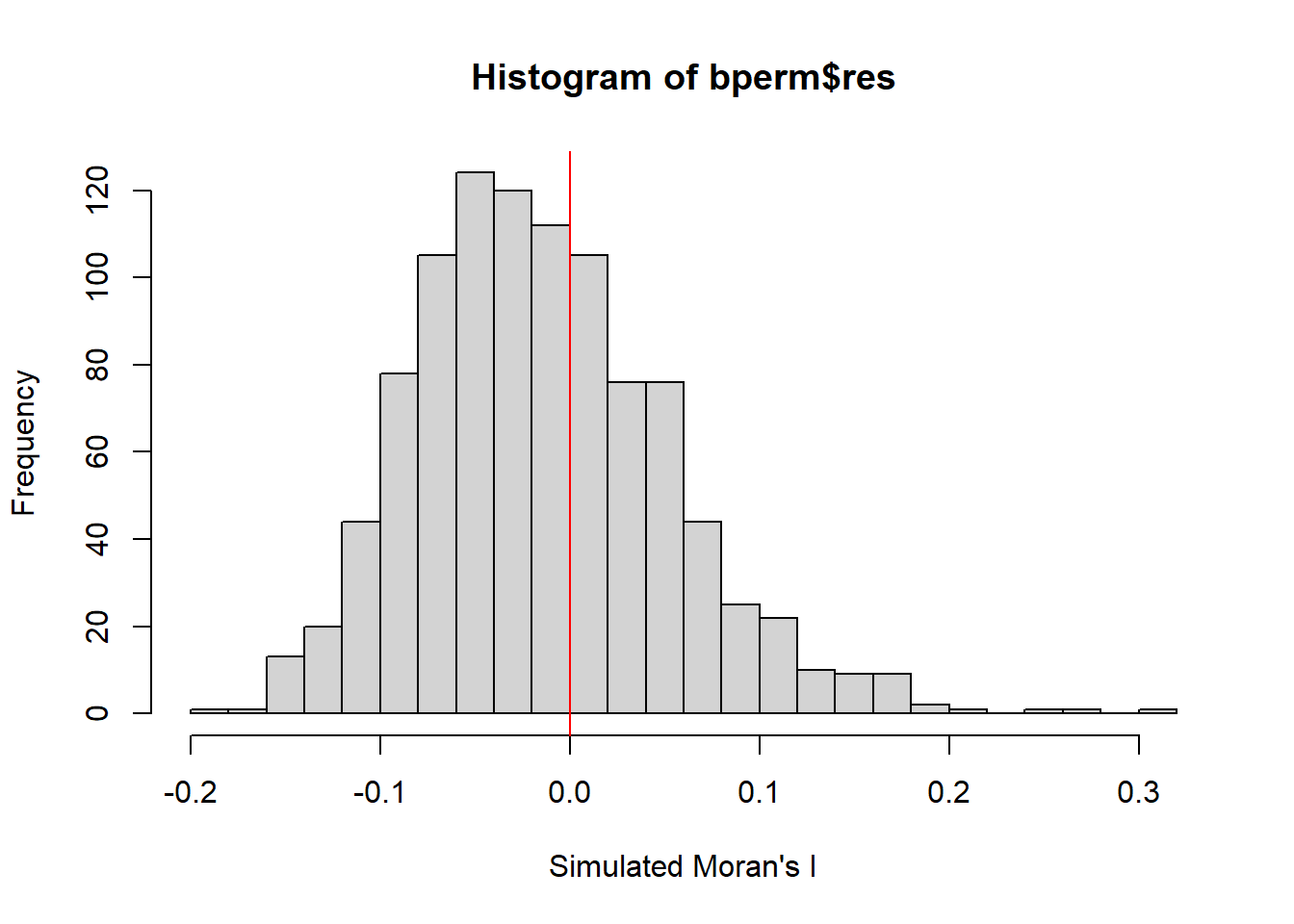

Moran’s I test require normal and randomised data and we can test that using Monte Carlo simulation. The simulation predicts the likelihood of outcomes based on random values. Here we use set.seed() to fix the random values so that we will obtain the same set when generating the random values. The p-value obtained will then be used to compare against the p-value of the actual p-value from the Moran’s I test.

We can also simulate using moran.mc().

set.seed(1234)

bperm= moran.mc(hunan$GDPPC,

listw=rswm_q,

nsim=999,

zero.policy = TRUE,

na.action=na.omit)

bperm

Monte-Carlo simulation of Moran I

data: hunan$GDPPC

weights: rswm_q

number of simulations + 1: 1000

statistic = 0.30075, observed rank = 1000, p-value = 0.001

alternative hypothesis: greaterBoth the actual test and simulated shows a small p-value, which means we can reject the null hypothesis of the Moran’s I test and we have sufficient evidence that there is an observed pattern or values of a region is affected by another neighbour.

Visualising the Moran’s I test

We can then plot the distribution of the simulated Moran’s I statistical test using a histogram.

mean(bperm$res[1:999])[1] -0.01504572var(bperm$res[1:999])[1] 0.004371574summary(bperm$res[1:999]) Min. 1st Qu. Median Mean 3rd Qu. Max.

-0.18339 -0.06168 -0.02125 -0.01505 0.02611 0.27593 hist(bperm$res,

freq=TRUE,

breaks=20,

xlab="Simulated Moran's I")

abline(v=0,

col="red")

Global Spatial Autocorrelation using Geary’s C test

Geary’s C test describes how features differ from their immediate neighbours. It uses a Geary C(Z value).

- If the Geary C value is larger than 1: the features are dispersed and observations tend to be different.

- If the Geary C value is smaller than 1: the features are clustered and observations tend to be similar.

- If the Geary C value is close to 1: the features are randomly arranged.

Relationship to Moran’s I test

Both tests have an inverse relationship to each other where a low C value and high I value can be seen when there is clustering of similar values. High C value and low I value can be seen when dissimilar values cluster.

C values range from 0 to 3 while I values range from -1 to 1.

Performing the test

Here we use the geary.mc() to perform the Geary C test.

geary.test(hunan$GDPPC, listw=rswm_q)

Geary C test under randomisation

data: hunan$GDPPC

weights: rswm_q

Geary C statistic standard deviate = 3.6108, p-value = 0.0001526

alternative hypothesis: Expectation greater than statistic

sample estimates:

Geary C statistic Expectation Variance

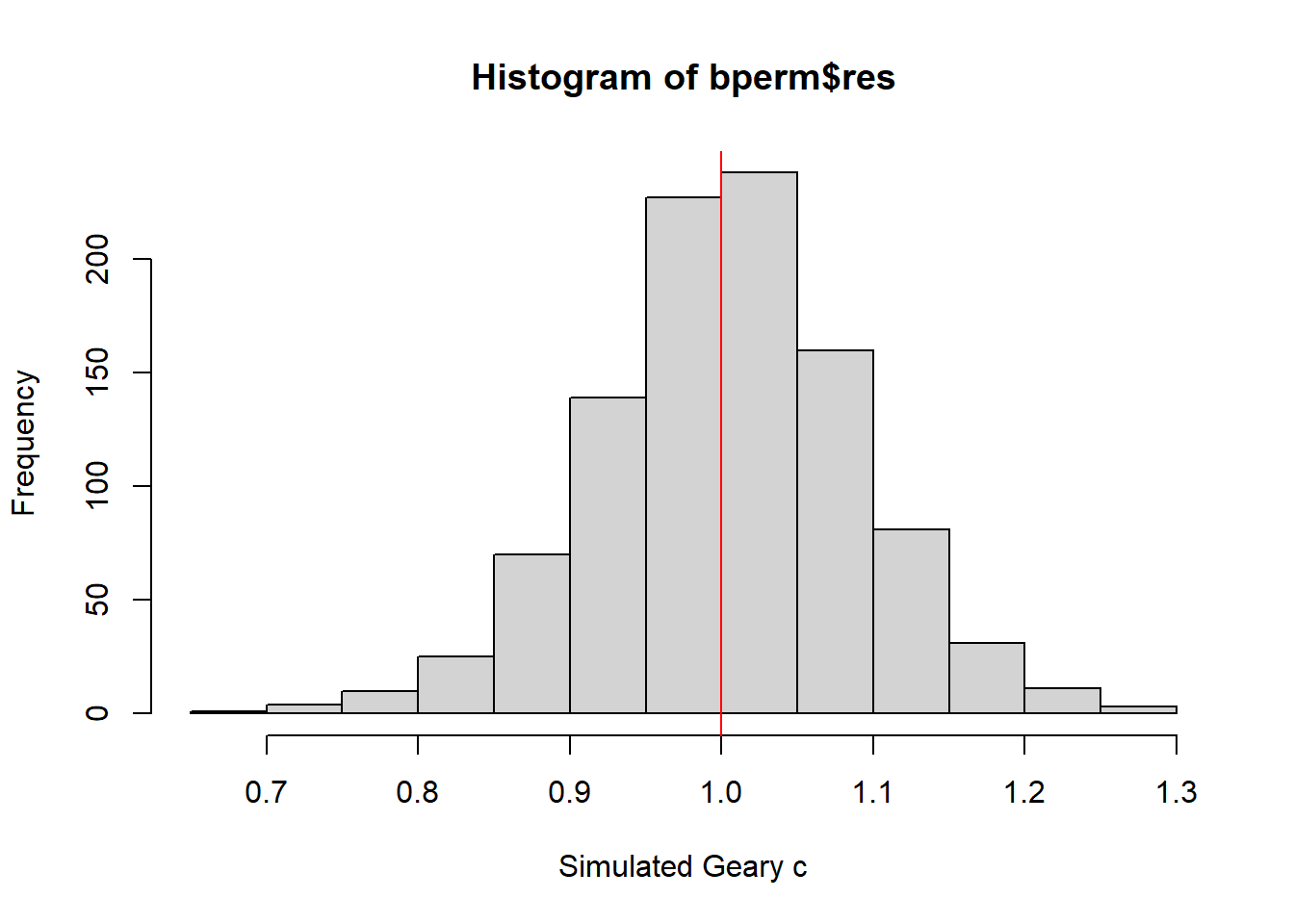

0.6907223 1.0000000 0.0073364 We can also perform a permutation test with a simulation.

set.seed(1234)

bperm=geary.mc(hunan$GDPPC,

listw=rswm_q,

nsim=999)

bperm

Monte-Carlo simulation of Geary C

data: hunan$GDPPC

weights: rswm_q

number of simulations + 1: 1000

statistic = 0.69072, observed rank = 1, p-value = 0.001

alternative hypothesis: greaterVisualising the Geary’s C test

We can then plot the distribution of the simulated Geary’s C statistical test using a histogram.

mean(bperm$res[1:999])[1] 1.004402var(bperm$res[1:999])[1] 0.007436493summary(bperm$res[1:999]) Min. 1st Qu. Median Mean 3rd Qu. Max.

0.7142 0.9502 1.0052 1.0044 1.0595 1.2722 hist(bperm$res, freq=TRUE, breaks=20, xlab="Simulated Geary c")

abline(v=1, col="red")

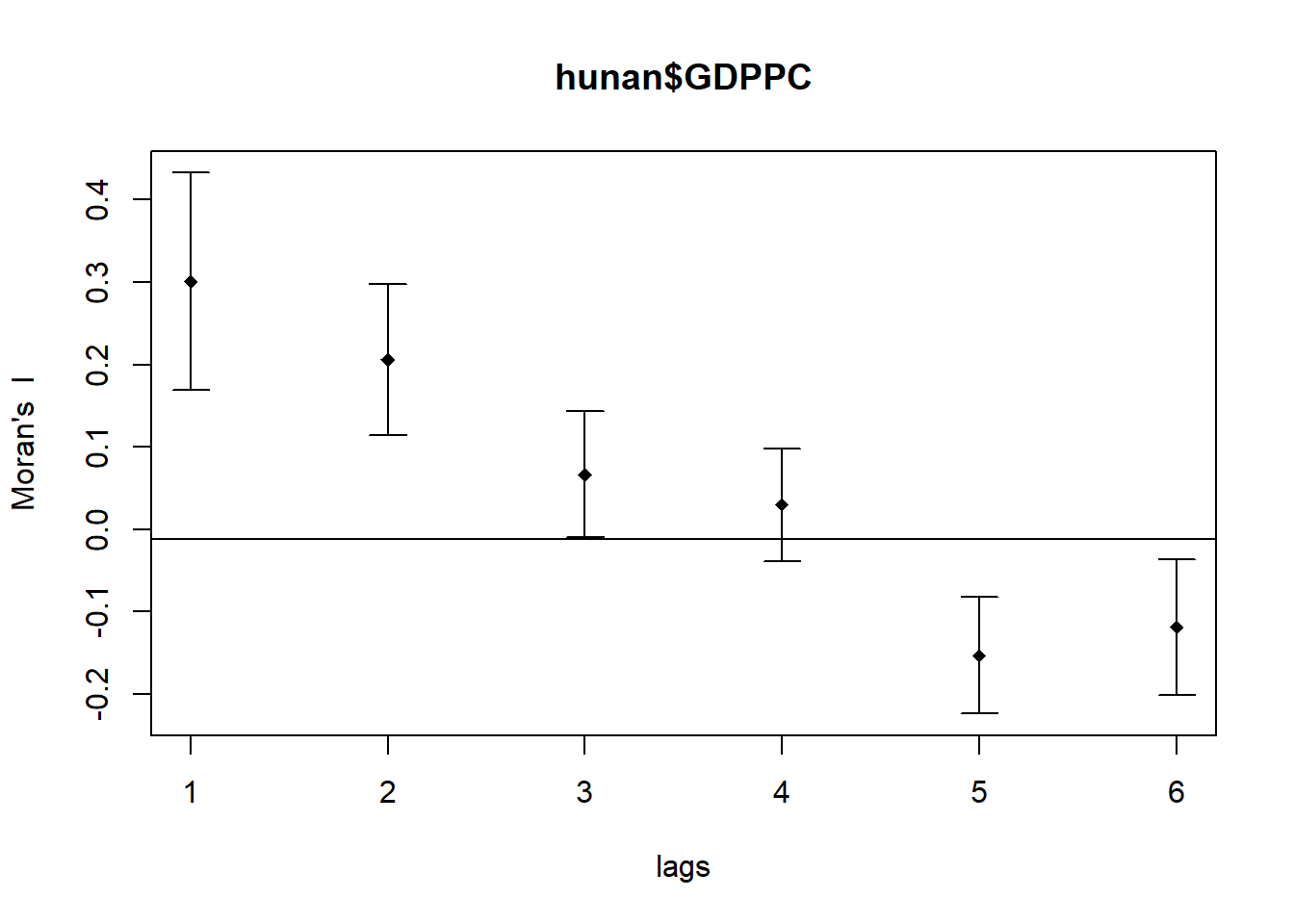

Spatial Correlogram

Here we examine the patterns of the Moran’s I and Geary’s C test. We can see the correlation of when distances are increased.

Moran’s I correlogram

We will use the sp.correlogram() for calculating the spatial correlogram of the devleopment of Hunan.

MI_corr <- sp.correlogram(wm_q,

hunan$GDPPC,

order=6,

method="I",

style="W")

plot(MI_corr)

print(MI_corr)Spatial correlogram for hunan$GDPPC

method: Moran's I

estimate expectation variance standard deviate Pr(I) two sided

1 (88) 0.3007500 -0.0114943 0.0043484 4.7351 2.189e-06 ***

2 (88) 0.2060084 -0.0114943 0.0020962 4.7505 2.029e-06 ***

3 (88) 0.0668273 -0.0114943 0.0014602 2.0496 0.040400 *

4 (88) 0.0299470 -0.0114943 0.0011717 1.2107 0.226015

5 (88) -0.1530471 -0.0114943 0.0012440 -4.0134 5.984e-05 ***

6 (88) -0.1187070 -0.0114943 0.0016791 -2.6164 0.008886 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1Geary’s C correlogram

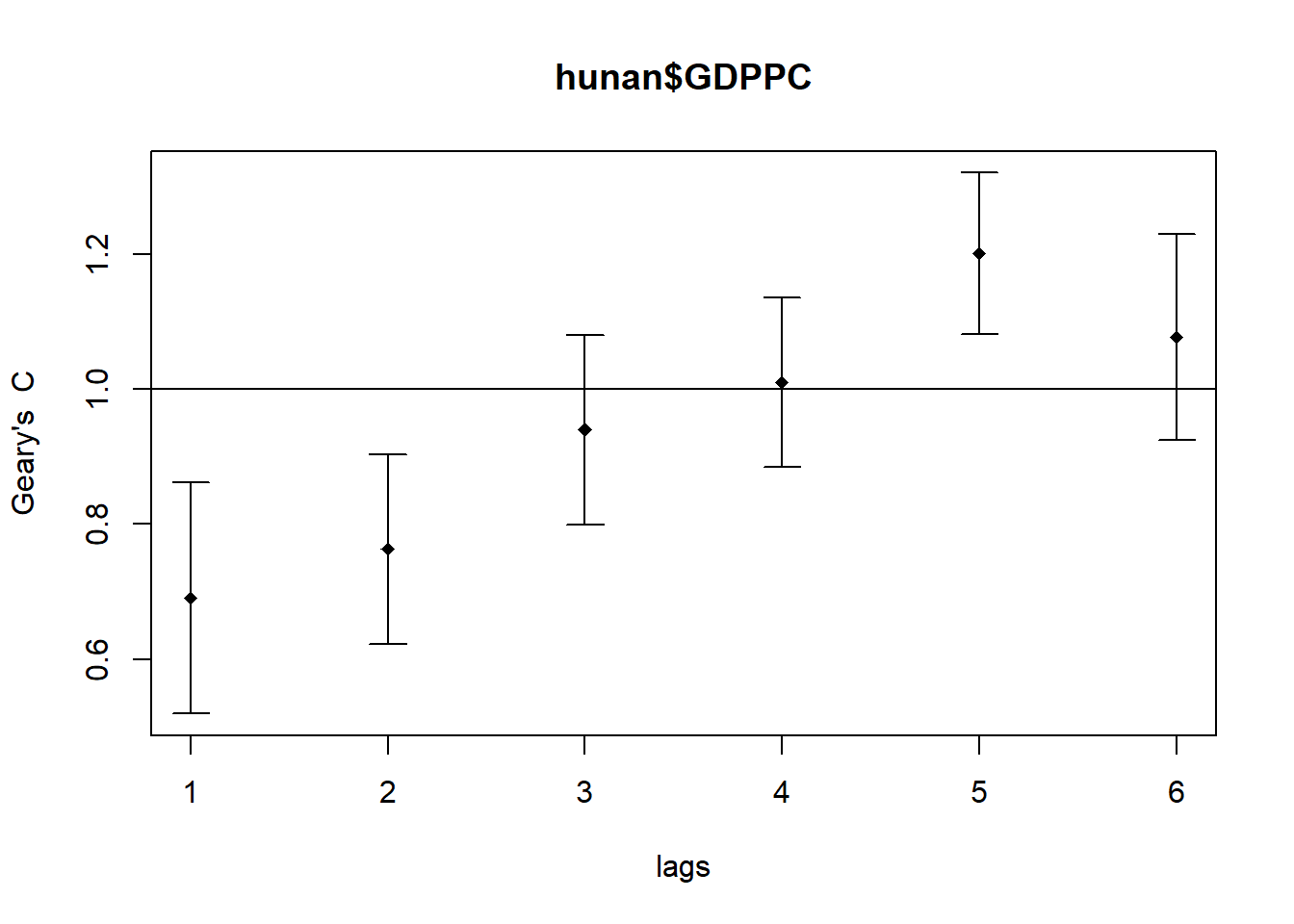

We will use the sp.correlogram() for calculating the spatial correlogram of the devleopment of Hunan.

GC_corr <- sp.correlogram(wm_q,

hunan$GDPPC,

order=6,

method="C",

style="W")

plot(GC_corr)

print(GC_corr)Spatial correlogram for hunan$GDPPC

method: Geary's C

estimate expectation variance standard deviate Pr(I) two sided

1 (88) 0.6907223 1.0000000 0.0073364 -3.6108 0.0003052 ***

2 (88) 0.7630197 1.0000000 0.0049126 -3.3811 0.0007220 ***

3 (88) 0.9397299 1.0000000 0.0049005 -0.8610 0.3892612

4 (88) 1.0098462 1.0000000 0.0039631 0.1564 0.8757128

5 (88) 1.2008204 1.0000000 0.0035568 3.3673 0.0007592 ***

6 (88) 1.0773386 1.0000000 0.0058042 1.0151 0.3100407

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1